Update May 2026: As of 20 April 2026, Go & Grow has launched as a standalone brand at goandgrow.eu, separate from Bondora. Bondora remains as the consumer lending business that originates the loans behind the product. Your account, login, and balance stay exactly the same.

I have had over €16,000 of my own money sitting inside Go & Grow for years. The platform offers a target potential return of up to around 6% per year, paid daily, with no lock-up period. It is not a bank deposit, your capital is at risk, and the up to ~6% rate is a target, not a guarantee. But for me it has played a very specific role in my portfolio, and after the April 2026 rebrand it felt like the right time for a fresh, honest 2026 update.

This review is based on real skin in the game, not a quick test deposit. I cover what changed with the rebrand, how the product works, the new Goals feature, a real story of when I had to pull thousands of euros out at short notice, and the risks you should understand before depositing.

What Actually Changed With the Rebrand

As of 20 April 2026, Go & Grow stands on its own as a refreshed standalone brand, separate from Bondora. Bondora itself remains and continues to run the consumer lending business that originates the loans behind the product. Two pillars, two focuses, room for each side to grow independently.

For anyone already using the platform, the important part is what did not change. Your account, login, balance, and history all stay exactly the same. There is nothing to migrate and nothing to re-verify. The target potential return is still up to around 6% per year, paid daily, with no lock-up period. Withdrawals still work the same way with the €1 flat fee each time. The loans powering the portfolio are still originated by Bondora in the background. Same engine, refreshed brand.

What did change: the website is now goandgrow.eu, the logo and visual identity are refreshed, and the emails you get from the platform are gradually moving from bondora.com over to goandgrow.eu addresses. So if you spot a slightly different look in your inbox or in the app, that is exactly why.

How Go & Grow Works

Bondora was founded in 2008 in Estonia, making it one of Europe's longest-running platforms of its kind. The Go & Grow product itself launched in 2018, so it just turned eight years old in 2026. This really is not a new project, it has been live and paying returns daily through multiple rate cycles, including the high-rate period when many investors (myself included) pulled cash out for safer options.

In practice, here is how the product works:

- You deposit euros into your Go & Grow account from any European bank you control

- Your balance is spread automatically across thousands of small consumer loans originated by Bondora in five countries: Estonia, Finland, the Netherlands, Spain, and Latvia

- You earn a target potential return of up to around 6% per year, calculated and paid daily (target, not a guaranteed rate)

- There is no lock-up period, so you can request a withdrawal at any time, subject to liquidity terms

- The minimum deposit is just €1, the only fee is a flat €1 per withdrawal

Important detail: this is not a bank deposit. There is no EU deposit guarantee scheme protecting your balance. That is the trade-off for the higher potential return compared to a regulated bank account, and it is the single most important thing to understand before you put money in.

Track Record and Platform Numbers

For context on scale and history, the official platform numbers as of July 2026 show roughly €2.16 billion invested, €192 million earned in returns across the lifetime of the platform, and more than 513,000 investors. Bondora has operated since 2008, while Go & Grow was officially released in June 2018.

On the regulatory side, Bondora AS is supervised as a licensed credit provider by the Estonian Financial Supervisory Authority, with the Finnish Financial Supervisory Authority and the Latvian Consumer Rights Protection Center overseeing their respective markets.

What the 2025 Financials Tell Me

Bondora Group had a strong 2025. Its audited accounts show €62.7 million in revenue, €9.5 million in net profit, €13.0 million in operating cash flow, €20.4 million in cash, and €27.5 million in equity. The group reported no interest-bearing liabilities at year-end, and KPMG issued an unmodified audit opinion. You can read the full 2025 annual report here.

These figures cover Bondora Group in 2025, before Go&Grow OÜ was separated from the group in 2026. The consumer-loan claims investors own also sit outside Bondora's balance sheet. A profitable, cash-generative originator helps, but it does not protect your Go & Grow balance from borrower defaults or delayed withdrawals.

The report puts the total loan portfolio at €697 million and describes €514 million as performing. It does not provide enough detail to treat the remaining amount as a forecast loss, but I would like to see a fuller arrears and recovery breakdown. I also think investors should know that Estonia's regulator fined Bondora AS €200,000 in April 2025 for responsible-lending breaches involving loans issued between December 2023 and February 2024. The fine does not threaten the group's solvency, but underwriting standards matter when investors carry the credit risk.

My Personal Experience: Over €16K Inside

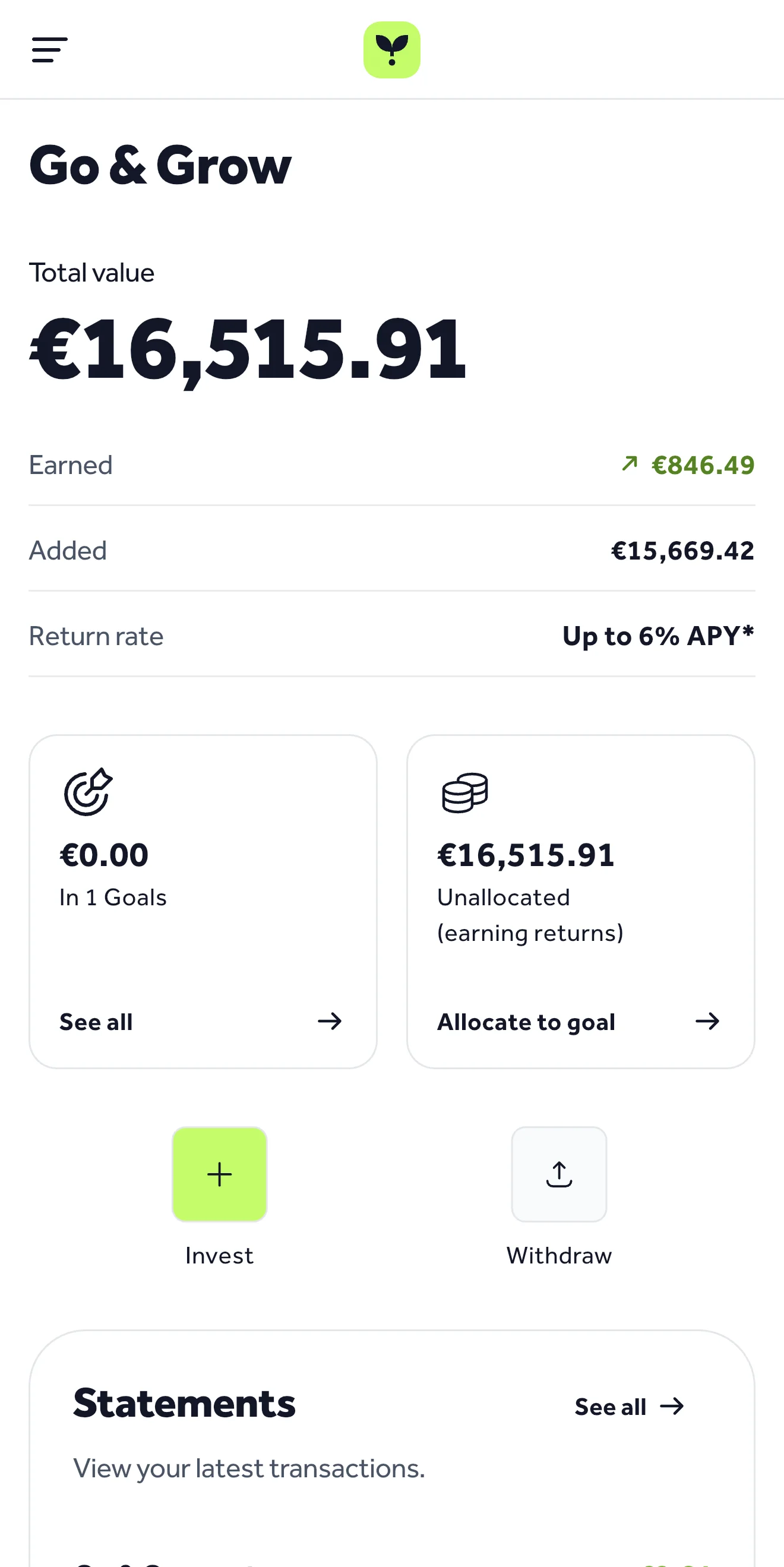

I have over €16,500 of my own money inside Go & Grow as of May 2026, made up of roughly €15,668 in deposits and €867 in returns compounded back into the pot. At this level I see a small return amount landing in the balance every day, and that number keeps creeping up as it compounds. There is nothing for me to do, it just shows up.

The whole experience is about as frictionless as it gets. I use the app to glance at the balance and the daily return, and the desktop site when I want a fuller view. Either way there is nothing to allocate, nothing to configure, no loans to pick. You deposit, it starts earning, and the daily return lands in your balance automatically.

Returns compound automatically, since every day's earnings are added to your balance and then earn returns themselves. Over a multi-year period that compounding adds meaningfully to the total. Just remember: this is a potential return, not a guaranteed rate, and unlike a regulated bank deposit it is not covered by any EU deposit guarantee scheme.

Liquidity in Real Life: The Spain Rent Story

For me, the ability to pull money out fast is probably the single biggest reason I use the platform. Let me give you a recent example. I was in Spain with my family, staying in a longer-term Airbnb that I had booked directly with the landlord. Rent was due, around €4,000, payable in euros by bank transfer (booking direct meant no card option).

The problem: most of my money lives in Dubai, where I am based, and a UAE-to-Europe bank transfer can sometimes take a few days. My Revolut euro balance was low because cash sitting there does not really earn me anything. The landlord was already chasing me for the payment.

What I did instead: I opened the Go & Grow app, hit Withdraw on a few thousand euros, and the funds were in my Revolut account literally a few minutes later. The rent was paid the same day. Later, when the UAE transfer eventually arrived in my Revolut, I just topped Go & Grow back up to where it had been before.

For me, that kind of speed on a meaningful amount is a genuinely strong feature, especially compared to having that cash sitting in a bank account at near-zero return. That said, it should be very clear: it may not always be possible to withdraw immediately. In that scenario, Go & Grow will make partial payouts of your total withdrawal amount rather than a single instant transfer. Personally that has never happened to me in years of using it, but it is mentioned in the terms and worth knowing exists.

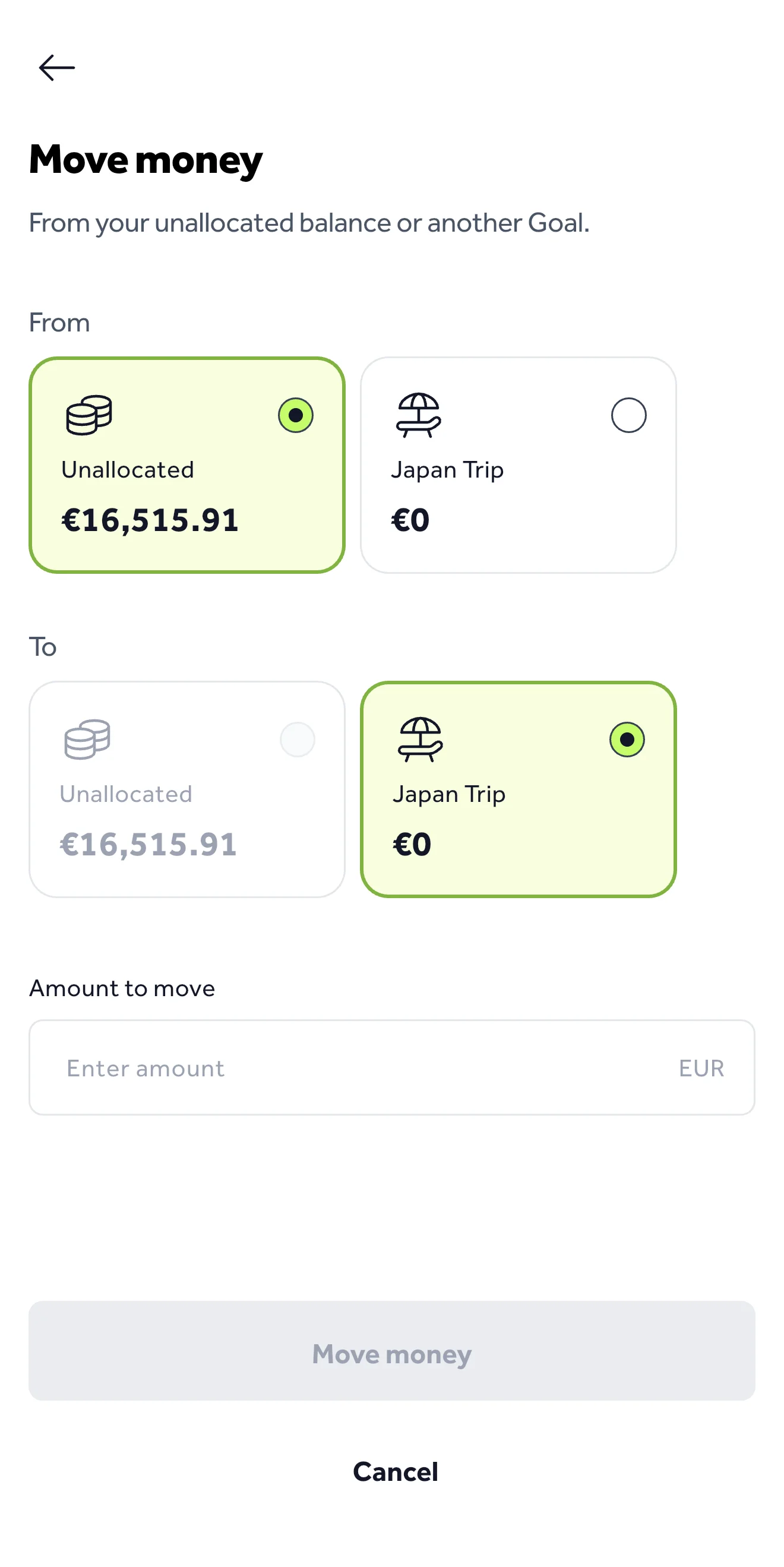

The New Goals Feature

Launched in April 2026, Goals is the first big product upgrade in a while. Inside your Go & Grow account, you can now create multiple Goals, name each one (a Japan trip, a new laptop, an emergency buffer), set a target amount, and move money between Goals or back to your unallocated balance with no fees and no friction.

The clever part: regardless of how you split the money across Goals, the whole balance still earns the same target potential return of up to around 6% per year, paid daily. You are not splitting your money into separate pots that each earn less. It is one pot, with Goals as a way to mentally organise the cash. Withdrawals still work from any Goal at any time, subject to the same liquidity terms as the main balance.

If you do not want to use Goals, you do not have to, the original single-balance experience is still the default.

Fees and Costs

Fees on Go & Grow are minimal, which is one of the things I like about the product. Here is what you actually pay.

There is no deposit fee, account fee, or annual management charge. The only standard fee is a flat €1 per withdrawal, regardless of how much you take out.

Risk vs. Reward

It is important to be transparent about the risks. Go & Grow is not a bank. Your deposits are not covered by any government deposit guarantee scheme. If the platform were to run into serious financial difficulty, you could lose some or all of your investment.

- Target potential return of up to ~6% per year, paid daily

- No lock-up period, withdraw any time (subject to liquidity terms)

- Minimum deposit of just €1

- Withdrawals typically fast in normal conditions

- Simple interface, nothing to configure

- Bondora operating since 2008, Go & Grow product since 2018

- Not a bank, no EU deposit guarantee scheme

- Underlying consumer loans can default

- Platform risk if Go & Grow fails

- Withdrawals may not always be immediate (partial payouts)

- Returns are taxable in your country of residence

- Only available in euros, not GBP

The up to ~6% target return reflects the higher risk profile of a non-bank platform. That is a trade-off each investor needs to evaluate based on how much capital they are willing to expose, and whether they can afford to lose it.

I treat Go & Grow as one slice of a diversified setup, not the only home for my euros. I keep a portion of my flexible euro cash here for the target return, and the rest in regulated bank accounts with full deposit protection.

How Go & Grow Fits in My Portfolio

For me, Go & Grow plays a very specific role. This is where I keep euros that I want to stay flexible, earning a target return while still being accessible if I need them fast. It earns on cash that would otherwise sit in a low-rate account doing nothing, it is accessible when I need it (like the Spain rent moment above), and it sits next to my stocks, ETFs, and broker accounts rather than instead of them.

I continue to top it up monthly, the same way you might dollar cost average into an ETF, just with euro cash instead of equity exposure. If you want to see how this fits alongside other asset classes in my wider setup, I cover that in my guide on 12 ways to invest your money in 2026. For my stocks side, my Trading 212 review covers the broker I use most for that.

Who Go & Grow Suits (and Who It Does Not)

Go & Grow is not a replacement for your stock portfolio or long-term investments. It works best for people who:

- Have euros they want to keep flexible, earning a target return rather than sitting idle

- Are comfortable with the higher risk of a non-bank platform (capital at risk, no deposit guarantee)

- Want daily returns without a fixed lock-up period

- Prefer a simple, hands-off product with zero loan-picking

- Are based in Europe and want exposure to consumer lending as a yield source

It is not suitable if you cannot afford to lose the money you deposit, or if you need the certainty of a government-backed deposit guarantee. Please read the full Go & Grow risk statement before investing.

*Target potential return, not a guaranteed rate. Capital at risk.

Frequently Asked Questions

Go & Grow is backed by Bondora's consumer lending business, which has been operating since 2008. It is not a bank, and funds are not covered by any EU deposit guarantee scheme. Your capital is at risk. It may not always be possible to withdraw immediately, in which case Go & Grow will make partial payouts of your total withdrawal amount.

In my experience, withdrawals usually arrive in your bank account within hours, sometimes minutes (see the Spain rent example above). However, it may not always be possible to withdraw immediately. In that scenario, Go & Grow will make partial payouts of your total withdrawal amount rather than a single instant transfer.

The minimum deposit is just €1, which makes it accessible if you want to test the platform before committing larger amounts.

No. The up to around 6% per year is a target potential return, not a guaranteed rate. Go & Grow has consistently maintained the target through multiple rate cycles since 2018, but actual returns depend on the performance of the underlying consumer loans and could change. Capital is at risk.

Returns are calculated and credited to your account daily. You can see the exact amount in your dashboard. Since they are added to your balance, they compound automatically.

Go & Grow does not withhold tax or file on your behalf. It provides a downloadable transaction and returns statement which you use when filing your own taxes. The exact tax treatment depends on your country of residence.

My balance is spread automatically across thousands of small consumer loans originated by Bondora in five countries: Estonia, Finland, the Netherlands, Spain, and Latvia. I do not pick the loans, the platform diversifies for me. The lending side is licensed and supervised by the Estonian Financial Supervisory Authority, with the Finnish and Latvian authorities overseeing their respective markets.

As of 20 April 2026, Go & Grow operates as a standalone brand at goandgrow.eu, separate from Bondora. Bondora itself continues as the consumer lending business that originates the loans behind the product. Your account, login, balance, target return, withdrawal terms, and underlying lending engine all stay exactly the same. What changed: the website, logo, visual identity, and email domain (gradually moving from bondora.com to goandgrow.eu).

Go & Grow is available to residents of most European countries. You can check the goandgrow.eu website for the full list of supported countries. The platform operates in EUR only.

Disclaimer: Capital at risk. The yield of investment of Go & Grow is up to around 6% per year, a target potential return, not a guaranteed rate. Go & Grow is not a bank deposit and is not covered by any EU deposit guarantee scheme. Before deciding to invest, please review the full risk statement and consult a financial advisor if necessary. It may not always be possible to liquidate assets or withdraw money immediately from Go & Grow. In that scenario, Go & Grow will make partial payouts of your total withdrawal amount, more on partial payouts here. This article contains affiliate links, meaning I may earn a small commission if you sign up through them, at no additional cost to you.