If you have been investing for a while, you know the feeling. You check your portfolio, and it is red again. The stock market is an incredible wealth-building tool over the long term, but in the short term, it can feel like a roller coaster. That is why I have been looking for something that complements my stock portfolio with steady, predictable returns. Something that pays me every single day, regardless of what the market is doing.

That platform is called Monefit SmartSaver. I have personally invested over 15,000 euros of my own money on it, earning around 3.11 euros per day at the time of writing, so this review is based on real skin in the game. I will walk you through exactly how it works, what it pays, what the risks are, and whether it makes sense for you as a European investor.

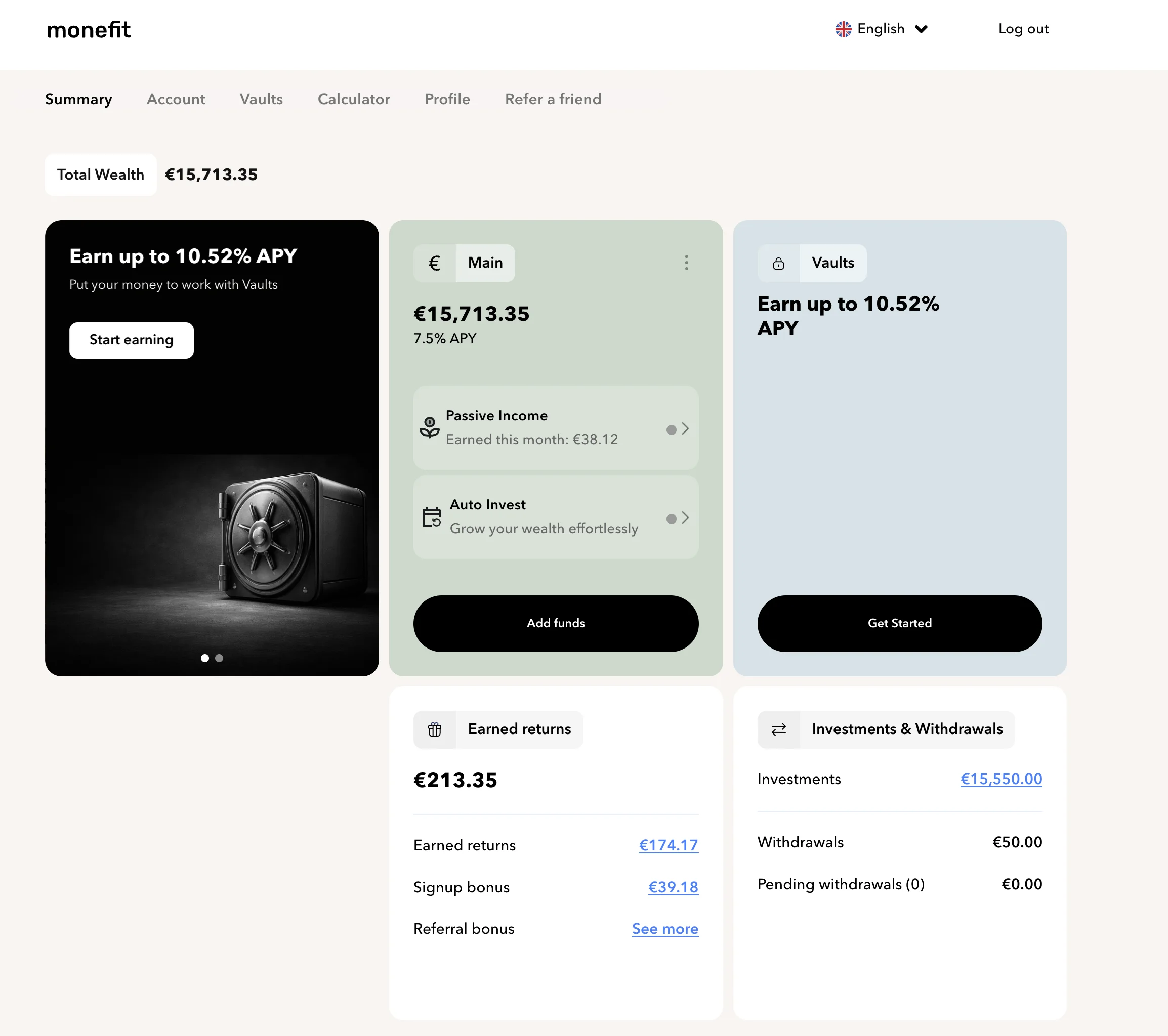

What Is Monefit SmartSaver?

Monefit SmartSaver is a platform where you deposit money, and it gets put to work by lending it out to real borrowers across Europe. These are consumer loans issued by a company called Creditstar Group. Borrowers pay interest on those loans, and you earn a share of that interest, calculated and paid out daily.

What makes Monefit different from traditional P2P lending platforms is that you do not have to pick individual loans. There is no auto-invest to configure, no loan ratings to evaluate. You just deposit your money, and the platform handles everything. Your funds get spread across many different borrowers and countries with individual loan caps to limit concentration risk.

If you have used other P2P platforms, you know that most of them require you to set up auto-invest strategies, filter by loan ratings, and manage your portfolio. Monefit takes care of all of that for you. Deposit, earn, done.

Who Is Behind Monefit?

Behind Monefit is the Creditstar Group, headquartered in Estonia. This is not some startup that appeared last year. Creditstar has been in the consumer lending business since 2006, giving them 20 years of operations. They have served over 1.4 million clients across eight European countries.

Their financials are audited annually by KPMG, one of the Big Four accounting firms. They hold over €52 million in equity and total assets exceeding €367 million. In 2024 alone, they generated €74 million in interest income. They have also won several industry awards, including Investment Tech of the Year in 2025 and recognition by Inc. 5000 as one of Europe's fastest-growing companies.

A long track record alone does not guarantee the future. But 20 years of audited financials is a much better starting point than a flashy website and a promise.

What Does It Pay?

There are two ways to earn on the platform: the main account and Vaults.

Main Account (Flexible)

Your money earns 7.5% interest per year, paid daily. You can access it whenever you want or need. Up to €1,000 per month is available instantly, and anything larger is processed within 10 business days.

Let me put this into real numbers. If you deposited €5,000 at 7.5%, that is roughly €375 a year, or just over €1 a day. Scale that up to €20,000, and you are earning about €1,500 a year, or €125 a month. That is a phone bill, a gym membership, or a monthly subscription to basically everything you use, covered entirely by passive income. And you have not touched your original €20,000.

Smart Saver Vaults (Fixed-Term)

If you can commit your money for a set period, Vaults offer even higher rates. They range from 12 to 24 months, with returns from 9.42% to 10.52% per year. The longer the commitment, the higher the return.

As of May 2026, Vaults shorter than 12 months are no longer available for new investments.

One important thing to know: if you need to close a Vault early, you lose all the accumulated returns, and there is a 30-day cool-down period before your funds are returned. So only put money into Vaults that you genuinely will not need for the full term.

Fees

I personally deposited the first week with my card because it was fast and convenient, then switched to bank transfers to save on the 1% fee. You can also set up auto-invest from your card, which is fee-free regardless.

How the Platform Works

The platform is currently desktop-only, with no mobile app yet. That said, once you set it up, it is essentially investing on autopilot. I check in on a monthly basis to see how much interest I have earned.

The interface is clean and straightforward. Depositing is as simple as clicking "add funds," choosing the amount, and selecting your payment method. You can also set up recurring auto-invest, which deducts money from your card on a schedule you choose, fee-free.

Once your money is in the main account, it immediately starts earning 7.5% interest. No additional steps required. If you want higher returns, you can create a Vault and choose your lock-up period.

Every day, your earned interest starts earning interest on top of itself. My own daily earnings have grown past 3.11 euros without any additional deposits, purely from interest stacking onto interest. That is the compound effect in action, and over time, it makes a real difference.

Withdrawals are also simple. Up to €1,000 same-day via bank transfer (avoid card withdrawals to skip the 1% fee). Larger amounts take up to 10 business days. You can also enable a passive income feature, available across the Main Account and all Vaults, that automatically pays out your accumulated interest to your bank account on the first of every month.

The platform also provides downloadable tax reports, which makes filing much easier. They do not report to tax authorities on your behalf, but giving you a clear breakdown of your earnings is a nice touch.

What Are the Risks?

Those daily returns do not come for free. There is a reason this pays more than a savings account, and you need to understand why.

- 20+ years of operations, KPMG-audited financials

- 100% withdrawal success rate since launch

- €52.7M in equity, 64% collateralized portfolio

- 4.6/5 Trustpilot rating from 1,000+ reviews

- Daily interest, fully hands-off management

- Not a bank account, no EU deposit guarantee

- Single counterparty risk (all funds go to Creditstar)

- No buyback guarantee or capital protection

- Not a regulated investment product

- Larger withdrawals can take up to 10 business days

First and most importantly, this is not a bank account. Your money is not covered by any EU deposit guarantee scheme. There is no €100,000 protection like you would have with a regular savings account. Those higher returns exist precisely because you are taking on more risk.

Second, there is single counterparty risk. All of your funds go to one group, Creditstar. Unlike some P2P platforms where you can diversify across multiple loan originators, here everything sits with one company. If Creditstar were to face serious financial difficulties, your investments could be affected.

Third, there is no buyback guarantee and no capital protection mechanism. If many investors withdraw at the same time, larger withdrawals might take longer to process. And Monefit SmartSaver itself is not a regulated investment product. Creditstar's lending entities are regulated in their respective countries, but SmartSaver operates as an Estonian entity outside of traditional financial regulation.

On the positive side, Creditstar has been profitable for over 20 years. Since launch, every SmartSaver user has received their money back with returns. The risks are real, but they are clearly defined. Knowing them is what allows you to make a smart decision about how much of your money belongs here.

Who Is Monefit SmartSaver For?

If you are in your 20s or 30s, already invested in stocks or ETFs, and have some extra cash beyond your emergency fund, parking it in SmartSaver instead of a savings account earning 2% could mean the difference between earning €200 and €750 on the same €10,000 over a year. That extra €550 goes right back into your portfolio. If you are looking for other ways to invest your money, this is one worth considering.

If you find the daily ups and downs of the stock market stressful, having a portion of your money in something more predictable can change how you feel about investing overall. When one part of your portfolio is growing steadily every single day, the volatility in other parts feels more manageable. For anyone just starting out, my guide to investing for beginners covers the broader picture.

But if you want 100% capital protection or you are uncomfortable with the idea that your money is not bank-guaranteed, then this probably is not the right tool for you. And that is perfectly fine.

How It Fits My Own Portfolio

I split my P2P cash allocation roughly 50/50 between Monefit SmartSaver and Go & Grow (formerly Bondora Go & Grow). Each platform plays a distinct role. Monefit is the yield engine, paying 7.5% on the flexible balance and up to 10.52% inside Vaults. Go & Grow is the liquidity buffer, paying a lower 6% but letting me withdraw any amount at any time, usually within a couple of hours. You can read my Go & Grow review for the full breakdown.

The reason I do not put everything into Monefit, even though the rate is higher, is the withdrawal structure. On Monefit, only 1,000 euros per month is available instantly. Anything larger takes up to 10 business days to arrive. On Go & Grow, I can pull the full balance at any moment, no limits. If I ever need quick access to a larger amount, I go to Go & Grow first. Monefit takes care of the higher long-run yield. It is about using each platform for what it does best.

Frequently Asked Questions

The flexible main account pays 7.5% per year, calculated and paid daily. Fixed-term Vaults offer higher rates ranging from 9.42% (12 months) to 10.52% (24 months).

Monefit is backed by Creditstar Group, which has over 20 years of operations and is audited by KPMG. However, it is not a bank account and is not covered by the EU deposit guarantee scheme. Your capital is at risk, and there is no buyback guarantee.

Up to €1,000 per month is available instantly. Larger amounts are processed within 10 business days. Vault funds cannot be withdrawn early without losing accumulated returns and waiting 30 days.

No. Monefit SmartSaver is currently only available to European investors and operates exclusively in euros.

Bank transfers are completely free. Card deposits are free during the first 7 days after sign-up, after which a 1% fee applies. There are no management fees or withdrawal fees via bank transfer.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. This article contains affiliate links, meaning I may earn a small commission if you sign up through them, at no additional cost to you. When investing, your capital is at risk. Monefit SmartSaver is not a bank account and is not covered by any deposit guarantee scheme. Past performance is not a guarantee of future results.