You pull up a stock you already own. It is at €200. You remember when you first bought it at €100. Your finger hovers over the buy button. Something in your brain says "too late, too expensive, wait for a pullback."

That thing in your brain has a name. It is called price anchoring. It is probably one of the most common investing mistakes I see, and it has almost certainly cost me more money over the years than any market crash ever has.

Why we all do this

Our brains are wired to compare. Whatever price we first saw a stock at becomes the invisible benchmark for "cheap" and "expensive" forever after. It does not matter if the company doubled its revenue in the meantime, hired 10,000 more people, launched new products, and grew earnings every quarter. In our heads, the original price is still the "right" price. Anything above that feels like overpaying.

The problem is that the company did not stop existing at the price you bought it. It kept growing. The stock price caught up. And if you are still anchored to your old mental benchmark, you sit on the sidelines watching a business you actually like compound without you.

The egg test

Here is the way I think about it.

You do not stop buying eggs when the price goes up. A year ago they were €1. Now they are €1.50. You probably grumble about it at the checkout, but you still put them in the basket. Because you need them, they are good for you, and refusing to buy eggs at €1.50 because they "used to cost a euro" would be genuinely weird behaviour.

But that is exactly how a lot of people treat their portfolios. They bought a stock at €100, now it is €200, and they refuse to add more on principle. Even though they still believe in the company. Even though they still plan to own it in ten years. Even though their monthly dollar cost averaging plan clearly says "keep buying."

Where stocks differ from eggs (and why it helps you)

Eggs do not earn money. Stocks do.

When an egg goes from €1 to €1.50, you are paying 50% more for the exact same egg. Nothing about the egg changed. It is just more expensive.

When a stock goes from €100 to €200, a lot can happen underneath that number. If the company was earning €5 per share when you bought, and now earns €12, the price doubled but earnings more than doubled. On a valuation basis, the stock got cheaper. Higher price, lower multiple.

Share price doubled. Valuation multiple got cheaper. This is the part most people miss. Share price alone tells you almost nothing. A stock at an all-time high can be a bargain. A stock 40% off its high can still be expensive. What matters is the price relative to what the business actually earns.

ASML, a real example from this month

ASML, the Dutch company that makes the lithography machines every chip fab in the world relies on, reported Q1 2026 earnings on 15 April. Revenue up 13% year over year. Net income up 17%. Earnings per share up 19%, from €6.00 to €7.15. They also raised their full-year 2026 guidance. The business is materially bigger than it was a year ago.

Interestingly, the stock actually slid after the print, because of new worries about China export curbs. Earnings up, share price down. That is the opposite of the trap this article is about, and the same rule applies in reverse. The share price does what it does. The math underneath is what I care about.

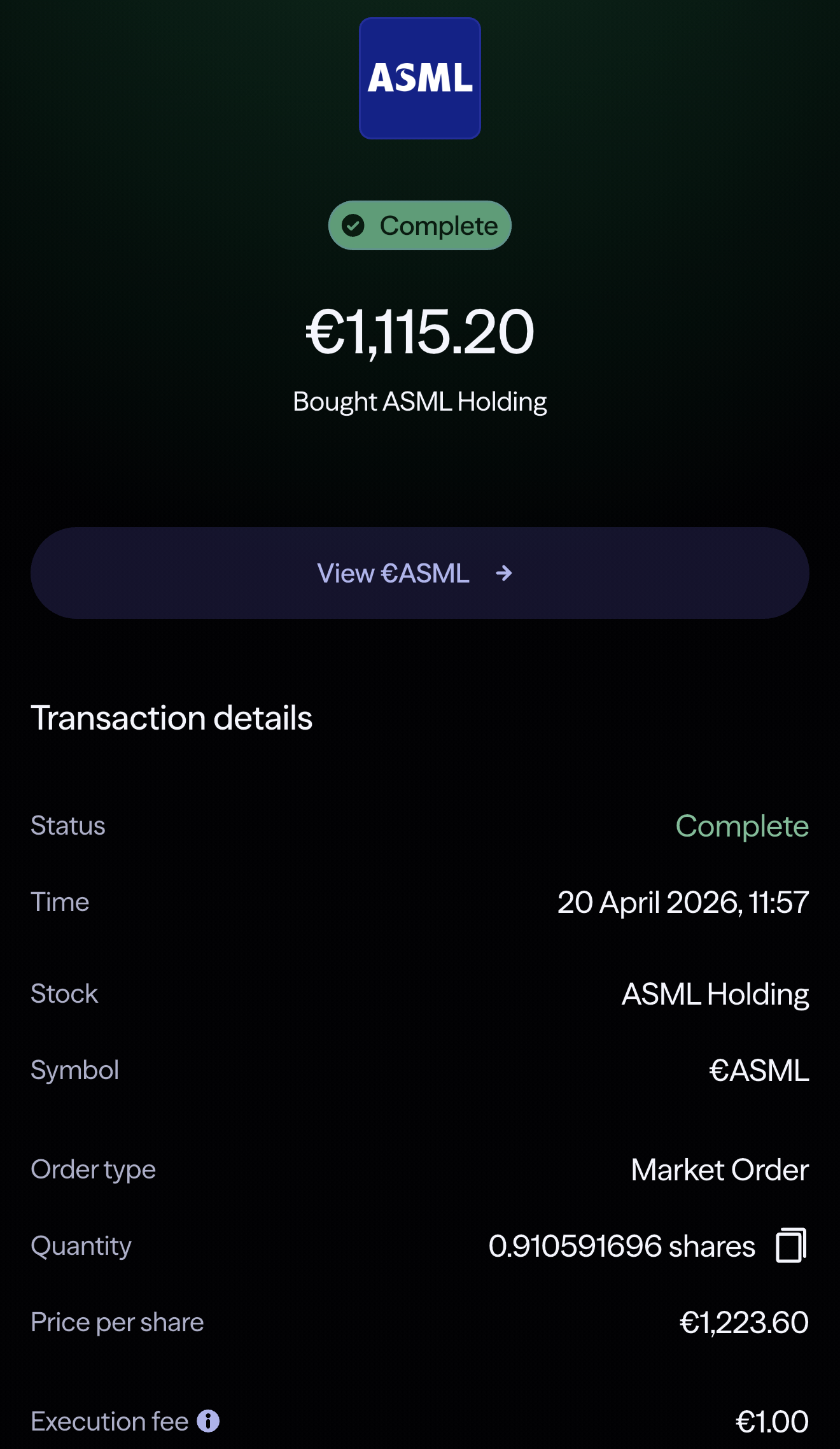

On Monday 20 April I added ASML to my portfolio for the first time. €1,115 worth, at €1,223.60 per share, through Lightyear in euros. Not the cheapest entry price I have ever paid for a stock. But ASML just grew its bottom line 19% in a single quarter. I am not holding it for the next three months. I am holding it for the next decade.

The sibling biases that make it worse

Price anchoring does not travel alone. It has a family of cognitive shortcuts that reinforce it, and once you see the pattern, you stop falling into all of them at once.

Loss aversion. We feel the pain of a loss about twice as intensely as the pleasure of an equivalent gain. That is why paying "more" for something we already own feels psychologically expensive, even when the math says we are getting a better deal. I have written about the emotional side of this in the context of watching a portfolio drop £52,000 in a week. The same wiring kicks in, just inverted, when prices are rising. It cuts the other way too, because refusing to sell a loser at a loss is the same anchoring instinct, which is the call I worked through when I sold a stock I still believed in.

Recency bias. We over-weight what happened in the last few weeks. If a stock just ran 40%, we assume it is "due" for a correction. If it just dropped 40%, we assume it is "due" for a rebound. Neither assumption has any basis in the business underneath. It is pattern matching on noise.

Hindsight bias. Once we know how a stock performed, we rewrite the story in our heads as if it was obvious. "I should have bought more when it was cheap." In reality, at the time it was "cheap" it also felt scary, which is exactly why you did not buy more. The next cheap-and-scary moment will feel identical. Your brain will not flag it as an opportunity in real time. It will flag it as a risk.

All three biases point in the same direction: away from sticking to a planned allocation and toward reactive decisions based on the last price you happened to see.

A simple decision framework

When I catch myself flinching at a higher price, I run through three questions before I let myself skip the buy.

- 1Is the business bigger than it was at my entry price? Revenue, profit, users, customers, market share. If yes, the higher share price might just be tracking real growth.

- 2Is the valuation multiple (P/E, P/S) higher than the company's own 5-year average, or its peers? If no, the stock is not actually expensive on any framework other than my memory.

- 3Would I start a new position today, if I had never owned it? If yes, then adding to my existing position is the same decision. My entry price should not change it.

Two yeses and a maybe, I keep buying. Three nos, I pause. One question I explicitly do not ask: "is the share price higher than last time I checked?" That is the anchoring trap the whole framework is built to bypass.

Signals that say keep buying, and signals that say pause

Price anchoring is about not freezing a plan that is working. It is NOT a green light to chase every rally or pile discretionary cash into a relief bounce. Here is the difference in practice.

- Your monthly DCA is due

- Business fundamentals are growing

- Valuation multiple is in line with history

- You would buy it today if you did not already own it

- Your investing horizon is 5+ years

- Valuation multiple is stretched vs history

- Earnings growth has actually slowed

- You are piling discretionary cash into a rally

- Your allocation is already overweight the name

- Your thesis has changed materially

If you own a name like Alphabet and it is up 60% since your entry, that is not by itself a reason to stop adding. Ask the three questions. Match the signals. If the business kept growing and the multiple is not extended, your DCA should keep going.

Where I buy European stocks

I bought my first ASML shares on Lightyear because, for European-listed stocks in euros, it is the smoothest and cheapest option I have used. Low commissions, proper euro accounts, and fractional shares, which matters for something like ASML where a single share is north of €1,200. You can buy €100 of it instead of needing €1,200+ to get started.

Lightyear: €100 welcome bonus

Sign up through my link or use code KAI. You will get up to €100 in a fractional share or ETF in your personal account.

The one-line summary

Look at the earnings, not the price tag. In ten years, what I paid for ASML last April will not matter. What will matter is whether I kept buying along the way, and whether the businesses I own kept growing. Those are the only two things I can actually control as a long-term investor. My mental anchor to an old entry price is not on the list.

Frequently Asked Questions

Price anchoring is a behavioral bias where the first price you saw a stock at becomes the invisible benchmark you compare every future price to. It makes stocks feel expensive even when the underlying business has grown, because your mental reference point is stuck in the past.

Yes, if the underlying business is still growing. All-time highs are not by themselves a reason to stop planned buying. What matters is the valuation (price relative to earnings), not the share price relative to your entry point. A stock at an all-time high can still be cheap on a valuation basis, and a stock 40% off its high can still be expensive.

Look at valuation multiples (price-to-earnings, price-to-sales, EV/EBITDA) relative to the company's own historical range and its peers. If the P/E today is lower than its 5-year average, the stock is cheaper than its own history, regardless of the share price. That is the only honest way to answer the question.

Chasing a rally is a discretionary timing bet, dumping extra cash into a short-term bounce because you feel late. Price anchoring is the opposite problem, freezing your planned monthly buying because prices are higher than your original entry. One is over-trading, the other is under-investing. The decision framework in this article is designed to bypass both.

ASML is a clean example of the thesis: a profitable, growing business where Q1 2026 earnings grew faster than the share price (earnings up 19%, stock actually down on China export worries). It is also a European-listed company in euros, which fits the new European stocks bucket I am building through Lightyear. The share price was not the cheapest I could have paid, but the business got bigger in the meantime, so the valuation is cheaper than it looks.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. When investing, your capital is at risk. You may get back less than you invested. Past performance is not a guarantee of future results. This article contains affiliate links, meaning I may earn a small commission if you sign up through them, at no additional cost to you.